Due to numerous changes in legislation, the issue of receiving a pension from the state is becoming increasingly relevant. Therefore, citizens are beginning to think about making independent contributions to the Pension Fund in order to obtain additional guarantees for its appointment. Such payments can add missing service and pension points, thereby making it possible to receive monthly payments upon reaching a certain age.

What is voluntary pension insurance

The concept of voluntary pension insurance is not disclosed by current legislation. Only in some regulatory documents (for example, the Tax Code) does the term non-state pension provision (hereinafter also referred to as NPO) appear, which in practice is a synonymous concept.

In simple words, it means entering into a voluntary contractual relationship with a non-state pension fund to form an additional pension to the state pension. After concluding such an agreement, the citizen or his employer has an obligation to make payments within a certain period of time in the amount established by the agreement.

All funds transferred voluntarily will form an additional pension in the future . Also, the specified finances can be moved from one management organization to another or received by the citizen or his heirs.

In addition to NPFs, voluntary pension insurance programs are also offered by insurance companies. In this case, an insurance contract is concluded, and the insured person or policyholder makes periodic payments towards a future pension.

Important! Non-state pensions are not regulated by separate legislation, and the procedure for its formation is determined by the internal rules of the NPF.

At the same time, the activities of the fund within the framework of voluntary insurance should not contradict the law.

Taxation of the self-employed

From January 1, 2020, Russians living in the Kaluga or Moscow regions, Moscow or Tatarstan can become participants in a pilot project to legalize independent activities under special conditions.

The essence of the experiment is:

- Freelancers work on a notification basis.

- Payment of taxes in the amount of 4% on income received from citizens, and 6% on profits from cooperation with legal entities.

- Installing a special application on your mobile device that will calculate income based on receipts.

- Making tax payments through the same application.

Important! Citizens who did not make a profit during a certain period are not required to pay tax for this time. A tax amount of 100 rubles or more is subject to payment. In other cases, the payment is transferred to the next period.

Self-employed people do not need to open a separate account to pay taxes. To do this, you can use any card, including an existing one, by linking it to a mobile application. Expenses will not be taken into account when calculating deductions. When paying taxes, taxpayers under a special regime do not have to provide financial statements.

Difference between voluntary and mandatory

The main differences between these two types of insurance lie in their very names. Mandatory implies the obligation of a citizen or his employer to make contributions to the Pension Fund for the future state benefit of an elderly citizen. The decision on voluntary insurance is made by the person himself or his employer; the state leaves the possibility of using this instrument at the discretion of these individuals themselves.

Within the framework of an NGO, a person entering into a contractual relationship with a foundation has the opportunity, at his own discretion, to determine:

- amount of payments;

- the duration of their transfer;

- frequency of application;

- formation scheme (inheritance rules, payment start period, etc.).

NPO rules are established by management companies independently, but must comply with the Standard Insurance Rules approved by the Central Bank. The specified rules of NPFs are registered with the Bank of Russia, and if changes are made to them, they are also subject to registration.

The role of the state in the formation of NGOs is to establish general legislative norms and regulate the activities of NPFs. The authorities do not directly participate in the formation of non-state pensions, since it is only additional to compulsory insurance.

Attention! Do not confuse NGOs with the voluntary transfer of additional insurance contributions within the framework of compulsory pension insurance. The latter is strictly regulated by the state, administered by the Pension Fund of the Russian Federation, and a separate legislative act was adopted as part of co-financing.

Legal framework for freelancers

The self-employed population refers to citizens who work on their own. These are entrepreneurs without hired employees who provide services independently or sell goods of their own production. This also includes farmers and other persons who act as both employers and employees.

Until now, such people worked exclusively for themselves, without paying taxes, and therefore without participating in the financing of the social sphere. They also did not pay contributions to the Russian Pension Fund, which means they could only claim a minimum pension provision in the form of a social pension.

A recent resolution of the State Duma of the Russian Federation determined the legal status for citizens receiving personal profit. Now nannies, photographers, caregivers and other freelancers will be able to legalize and work legally. One of the most important conditions is to notify tax authorities about the conduct of such activities.

Goals and functions of voluntary insurance

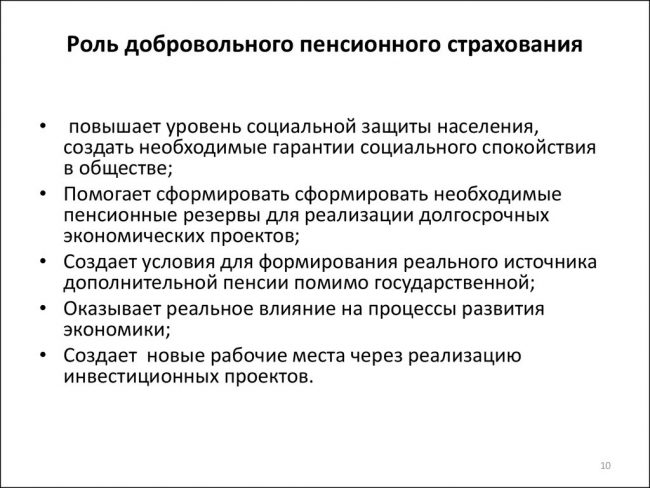

The main goal of voluntary pension insurance is to generate additional income after a citizen stops working due to age. An NGO allows you to have an additional source of monthly income along with government support. Also, this tool allows you to provide a citizen with a more decent financial condition in old age.

One of the functions of NGOs can also be investment of funds, i.e. their investment with the aim of making a profit. Thus, some NGO programs imply not only the possibility of transferring funds accumulated in this way to other funds, but also receiving them for further personal disposal. With the right choice of fund, its investors have the opportunity to accumulate a certain amount, as well as increase it in the case of financially competent activities of the NPF.

This type of insurance also makes it possible for citizens who work in harmful or dangerous jobs to retire before the deadline established by law. Early NPO allows citizens to receive a guaranteed monthly income before becoming eligible for payments from the state, while ceasing their work activities.

Another function is the provision of additional social guarantees to employees by the employer. Thus, a collective agreement between an organization and its employees may provide for the employer’s obligation to additionally insure employees within the framework of NPO. Thus, the employer can interest citizens in entering into labor relations with him, and the employee can receive additional guarantees.

In what cases are contributions to the Pension Fund justified?

If the self-employed pay contributions to the Pension Fund , they will be credited with the length of service that a person earns while in an official job under an employment contract. The insurance period also does not disappear; on the contrary, it increases, which is reflected in the size of the pension. This is beneficial for young people who have not yet found themselves in life, do not want to register a company, or cannot officially go to work in their position due to health conditions. Pensioners who are already receiving an old-age pension do not have any pleasure in giving up the lion's share of their earnings to increase their well-being.

Subjects of voluntary insurance

Within the framework of the NGO agreement, several categories of persons enter into relations, i.e. subjects of these legal relations:

- A non-state pension fund is an organization that provides the service in question by accepting contributions, investing them in various projects and areas, and paying non-state pensions to current pensioners or other persons entitled to this in accordance with the terms of the contract.

- Depositors are persons who make regular payments towards the formation of an NGO. These persons can be citizens themselves, as well as their employers. The category of the latter does not matter; both organizations and individual entrepreneurs who carry out their activities without forming a legal entity can act in this capacity. These persons always act as the second party to the NGO agreement.

- Participants are those citizens in whose interests contributions are made within the NGO, i.e. in fact, future recipients of non-state pension payments. If a citizen makes contributions on his own behalf and in his own interests, he will simultaneously be both a participant and a contributor.

Management companies that directly invest accumulated funds can act as independent subjects of legal relations under NGOs.

Subtleties of the DS agreement

The content of the agreement of the type of DS in question is established by each fund independently, taking into account the norms of the law. The form of such a document can always be viewed on the official website of a particular NPF before its conclusion or a visit to the company’s office.

At the same time, the standard form of this document is planned to be approved in the near future by the Directive of the Central Bank; its draft is currently being reviewed and discussed.

So, what you should pay special attention to in the DS agreement:

- Selected pension scheme. Each NPF offers different schemes for the formation and payment of non-state pensions in terms of the procedure for making contributions, receipt of savings amounts by the participant or his legal successor, and the time of appointment of the NPF. In the text of the agreement, as a rule, only the number of such a scheme is indicated, but its decoding is given in the Rules of a particular fund.

- Grounds for the emergence of the right to receive monthly payments within the framework of NGOs.

- Rules for making contributions (their size, frequency, length of time for making contributions).

- Period of validity of the contract.

The treaty in question concerns a very important area, and therefore is subject to careful study in its entirety. This applies not only to the stated points, but also to all other sections, be it the rights and obligations of the parties, their responsibilities, the subtleties of succession, etc.

DS programs at NPFs

In addition to compulsory insurance, each NPF offers NGO programs. Moreover, one can also take part in such a program according to various schemes approved by the internal rules of the fund. Each of them has a different list. GAZFOND, for example, offers 7 possible participation schemes; NPF Transneft already has 10 such schemes.

In each case, they are subject to individual study depending on the specific situation, the goals of investors and participants.

The differences between these schemes lie in the following criteria:

- duration of pension payments;

- the time of the participant’s right to receive a monthly income within the framework of the NGO;

- level of employer and employee participation in the program;

- the amount of contributions, duration and frequency of their payment.

A complete list of programs and schemes of a particular fund must be given in its pension rules, approved by the Board of Directors. Any citizen should be given free access to familiarize themselves with them.

In conclusion, we note that voluntary insurance within the framework of NGOs allows citizens to independently create an additional source of income in old age. DS serves not only to increase the future income of the pensioner, but can be considered as an investment or an additional guarantee to the employee on the part of the employer. When concluding an agreement, it is necessary to responsibly choose a scheme for the formation and payment of NGOs.