The main feature and task of the state is the implementation of fiscal functions. Current legislation provides for various types of tax payments that both citizens and legal entities are required to pay.

One of the most widespread fees is the personal income tax or personal income tax. It, as its name suggests, is paid by citizens upon receipt of any income in the amount of 13% of it.

If the taxpayer is employed, then this fee is deducted from the salary and transferred to the tax service by the employer's accounting department . If a citizen receives income not related to work, then he has a corresponding obligation to pay the tax himself.

Personal income tax belongs to the category of local taxes, funds from the payment of which are directed to the needs of specific territories. This should include education, security, social benefits, infrastructure development, and so on.

However, the specifics of taxation and exemptions from it are established by federal legislation. In particular, the Tax Code specifies certain grounds on which citizens can receive paid payments back or are completely exempt from them.

What is a tax deduction

A tax deduction should be understood as a certain part of a citizen’s income that is not taxed. In addition, the same term refers to the return to the taxpayer of a previously paid fiscal tax.

At its core, a tax deduction is a certain benefit that is provided to citizens in the presence of special circumstances. More details about them can be found in Art. Art. 217-221 of the Tax Code of the Russian Federation.

The most common reasons are:

- purchase of housing;

- tuition payment;

- treatment;

A tax deduction can only be granted if there is taxable income in a particular period. If there is no income, a deduction cannot be provided.

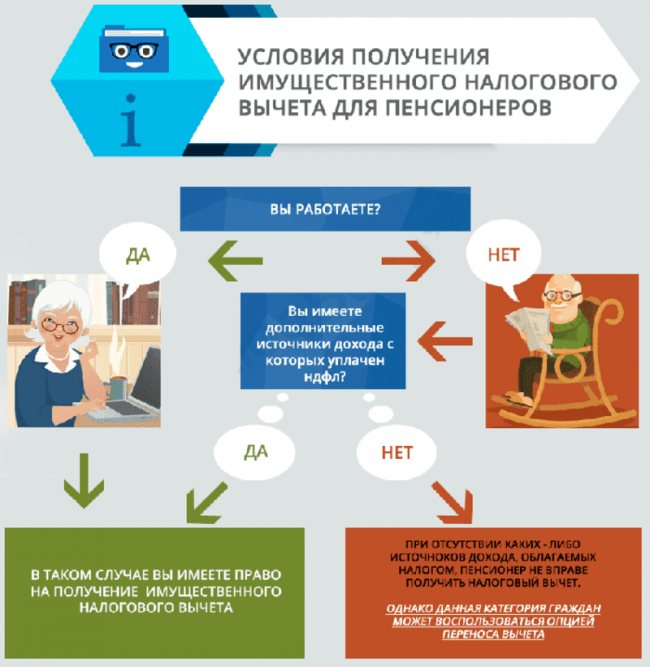

Can a non-working pensioner receive a tax deduction when buying an apartment?

There is a fairly well-established opinion that only those citizens who are officially engaged in working activities can claim tax benefits for the payment and return of personal income tax. However, this is not the case, despite the fact that, indeed, for the most part, personal income tax payers. persons are employees employed in various organizations.

The fact is that the deduction is provided to all eligible citizens who had taxable income for a certain period and, accordingly, fulfilled their obligations to the Federal Tax Service.

Attention! Non-working people may also qualify for a tax break on real estate purchases if they received income and then paid tax.

In addition, pensioners have the right to the so-called transfer of deductions. He assumes that it is possible to return tax for three tax periods preceding the purchase of an apartment. Therefore, if the pensioner was working at this time, he will receive a refund even though at the time of filing the application he is not working and has no income other than a pension.

Both working and non-working pensioners can count on the benefit, but only those who are not working at the time of submitting the relevant documents to the tax service have the right to transfer.

Are pension payments taxed?

In neighboring Ukraine, until recently the government levied a tax on citizens' pensions as if it were income. A reasonable question arises: will the Russian parliament make a positive decision in favor of this direction? We need to pay attention to the practice of other states. Thus, in Greece, as well as in a number of Baltic states, tax collections are also observed on citizens’ pensions.

The Russian Federation is not yet going to “encroach” on the pension provision of its own residents. Both the insurance part of the pension and the funded part are not subject to taxes. Even if the funded part of the pension is sent to a non-state pension fund, in this case the finances are not subject to taxation.

Only in a situation where the main employer enters into an agreement with a non-state pension fund to allocate the funded part of the pension of its own employees, then this income is subject to taxation.

As for the specifics, you can find out whether there are any tax breaks for working pensioners or those who have left work in your region directly from local services.

How to apply for a deduction

Despite the fact that a significant portion of citizens have the right to deduction, many of them are in no hurry to take advantage of it and do not receive the money they are entitled to. This is largely due to the fact that most of them are not aware of the opportunities associated with tax benefits.

In addition, many believe that the procedure for obtaining a tax deduction is quite complex and time-consuming and, thus, voluntarily refuse the opportunity to receive money, saving time and effort.

In fact, the procedure for applying for benefits is not particularly complicated, but it is quite lengthy in terms of time. Let's consider this issue in more detail.

Rules for filling out the declaration

To count on receiving a tax deduction, a citizen must draw up a special document - a declaration. This is a strictly unified paper that has a prescribed form - 3-NDFL. The document contains the personal data of the taxpayer, as well as information about the income received and the exact calculation of the benefit.

Important! Form 3-NDFL is subject to minor adjustments every year. If a declaration is submitted in an out-of-date form, it will not be considered.

The document itself structurally consists of several blocks, which indicate information about the taxpayer, the income received for a specific period, the calculation of the deduction, as well as the volume of the tax base and the amounts of tax that were paid to the budget.

The algorithm for filling out the declaration is as follows:

- Filling out the title page.

- Filling out “Appendix 1”, which indicates the total amount of income received.

- The required deduction is calculated in “Appendix 7”.

- “Section 2” is filled in with the calculation of information on the payer’s obligations.

- Filling out “Section 1”, which indicates the amount of the required deduction.

In addition, the declaration contains annexes that indicate the citizen’s sources of income, as well as some other information.

What documents need to be provided besides the declaration?

Pensioners have the right to count on a deduction on a general basis, which is why the procedure for registering it is the same as for other categories of citizens.

To receive this benefit, a citizen must provide a package of documents containing the following papers:

- declaration in form 3-NDFL. This document is submitted for a specific tax period. If a pensioner plans to receive deductions for several at once, then the number of declarations must correspond to the number of periods;

- information about the ownership of housing (certificate, extract from the Unified State Register of Real Estate, purchase and sale agreement, etc.);

- information on wages for past periods (2-NDFL certificates);

- a pension certificate or a certificate from the Pension Fund of the Russian Federation in the prescribed form, issued in exchange for it;

- marriage certificate, if the deduction will be distributed between husband and wife (if necessary);

- application in the established form (issued by the Federal Tax Service inspection).

In some cases, tax officials may require additional documents.

Where to contact

The declaration and accompanying documents should be submitted to the tax office at the citizen’s place of residence. Responsible specialists will check the completeness of the collected papers on site and also advise on additional questions that arise.

However, tax offices are quite busy institutions, and therefore filing a return can take a lot of time and effort. In this regard, it is possible to submit the necessary documents online.

For these purposes, the taxpayer’s personal account on the Federal Tax Service website is used . To do this, you need to register there, confirm your identity, and then create an electronic signature.

After this, the corresponding scans of documents are uploaded to the site, which must be certified with the created electronic signature.

Features of personal income tax return for pensioners

Without any special features, while maintaining standard technology, a tax deduction is provided for pensioners in 2020 if they do not quit their jobs, but continue to work as before. The situation is the same when they go to work under an agreement or contract. A special option for compensation payments from the state is the transfer of deductions from previous periods.

Property tax deductions are issued for purchased property in parts or the entire amount without differentiation into periods. The latter scheme may be used if the maximum amount of compensation allows it. You are allowed to receive money for a newly purchased house, for residential square meters that became property several years ago. At the same time, a specific period for registering property is not specified, but there is a maximum maximum for filing an application for reverse payments.

The main condition is that taxes be paid. Money in the form of compensation for funds spent on a purchase is issued by the fiscal service even when the citizen is not actively working at the enterprise. If the deadline for the implementation of compensation payments has not passed, the pensioner has the same grounds for this assistance from the state as an ordinary employee of a company or state-owned enterprise.

The applicant calculates compensation and indicates the current year 2020 as the starting year for recalculating obligations to the state.

The law allows the return of personal income tax money no more than three years from the date the applicant ceases paying fiscal contributions. In this case, this means retirement or transition to unemployed status after retirement.

It is not necessary to receive payment for going to work every day. Money is also declared from indirect profits. Any person who has rented out a garage, part of a house, or land can use the system of budget discounts and receives money drawn up under an agreement and with the payment of deductions.

In addition to rental relations, the same list includes resources that a citizen receives in the form of income to an account or in cash for a transaction for the sale of housing. This may also be the sale of other objects that are subject to personal income tax.

If the calculation of the refund is made by the enterprise or company where the pensioner works, then they can independently recalculate the application and coordinate all further actions to reduce the citizen’s taxation directly. That is, the fiscal service and accounting department of the enterprise then operate.

The only action required from the applicant is to submit information in the form of an application and calculation. It requires you to indicate your amount of compensation, according to the amounts submitted to the tax office for the purchase/sale transaction. There may be other cost options:

- repair estimate;

- estimate for the design and reconstruction of the building with mandatory transfer to the status of premises suitable for living.

How to get a deduction when buying an apartment for a working pensioner

How to get a tax deduction when a person has already earned a pension, but is in no hurry to stay at home and continues to work?

The law establishes that the main criterion for processing payments is the availability of deductions. The social status of the applicant in this case does not matter. That is, working pensioners undergo the same usual recalculation of income tax when buying an apartment as working people. The legislation does not differentiate between recipients of reverse payments by belonging to the category of working or non-working.

The norm prescribed in the legislation is addressed to all categories of residents (permanently residing in the Russian Federation) and paying a thirteen percent rate of personal income tax.

The refund accrual is carried out by the fiscal service upon personal application and after registration of such paper (electronic version) with the fiscal authority. After this, you will need to contact the company. There, a deduction is made in the form of salary growth and mutual settlement between the employer and the state.

You can receive compensation yourself after the tax service has decided to grant a discount.

How to get a tax deduction when buying an apartment for non-working pensioners in 2020

Let's look at how to return 13 percent from taxes for a non-working individual. And at the same time, the applicant made a significant purchase with accumulated funds? Two possible situations should be distinguished:

- the applicant has only the money that the state gives him as pension social security, and the recipient does not have a job in public or private commercial structures;

- There is money from the state (pension), and indirect income or salary from a registered place of work.

A non-working citizen must determine the payment period - it should be no more than three years. In this case, the period of acquisition of real estate is not taken into account and should be a reasonable limit. The property is registered only in the name of the person submitting the documents, that is, the applicant, for a reverse amount from the budget.

In practice, this would look like this for those retiring in 2019:

- payment period is no more than three years from the date of filing the declaration in 2020 - for 2019–2017 inclusive;

- money is withdrawn from the current accounts of treasury services and transferred to a specific applicant;

- Data verification can take from one to several months.

Can a non-working pensioner count on a reverse payment if he became the owner of real estate five years ago? Yes, he can, but only if he remained a tax payer no later than three years ago.

A working citizen who has reached the age at which he has the right to go on vacation based on his length of service and insurance payments, his status does not differ from that of an ordinary worker. His employment relationship must be formalized, and both wages and the amount of tax deductions established by law must be accrued for the work.

What is paid in the form of pension proceeds will not be included in compensation calculations. This money is issued directly by the state, without deductions on income from individuals. Let us remember the previously stated rule - deductions go only with personal income tax. Therefore, a pensioner or other recipient of social assistance should not count on such a refund.

The exception would be when a citizen has another way to earn money, and it is officially registered.

Receiving a property deduction if you have additional income

Let us clarify the position on the situation when a property deduction when purchasing land or an apartment can be carried out from indirect income:

- leasing, with the execution of an agreement and payment of taxes, a garage, summer house, other property, for example, cars, equipment and commercial premises;

- there is an officially registered receipt of income in the form of payment for a real estate asset provided in installments;

- funds from the fulfillment by the parties of the agreement with the full implementation of all tax deductions.

When a pensioner who combines work and pension status buys an apartment, he receives a full standard compensation rate of 13% with personal income tax.

As in other circumstances, the applicant must contact the fiscal service and the employer (if there is one) to implement the payment mechanism.

A working pensioner stopped working

Can a pensioner receive tax benefits if he is not registered as working? Or, if his work contract is terminated at the time of filing the declaration? Or if he retired not in February, but, say, in June? And one more important question: can ex-employees receive a tax deduction not partially, but completely?

For the legislation, such nuances do not matter, since two conditions remain fundamental - the availability of payments in the previous period, and the opportunity to take advantage of personal income tax benefits.

That is, if there is an acquisition this year, it is necessary to systematically prepare for filling out the declaration in 2021. This is when the period begins when it is possible to reserve a reverse payment.

The right to receive reverse payments always works if there were payments in the previous period for tax obligations. A non-working person receives a tax discount on the purchase of an apartment after verification of data by the fiscal service and submission of a declaration. It is necessary to justify the fairness of the deduction. If there are no gaps in the length of service and personal income tax payment, then the payment can be postponed for no more than three years. That is, in the fourth year from the date of the last payments, the pensioner can receive compensation.

Typical life situation: the applicant retires three years ago, and does not mind receiving reverse additional payments. The first requirement has been met - the time limit has not been exceeded. The second requirement is maintaining resident status (non-residents pay a different rate). That is, the applicant must reside in Russia for at least ½ year.

The third important point is that it is necessary to submit three declarations based on the results of previous periods. This allows the fiscal service to assess the financial situation and the legality of charges for such a transfer from the budget.

Deduction for the purchase of housing in common ownership of retired spouses

Is housing compensation due if one of the spouses has the opportunity to receive limited compensation, but the other does not? Yes, the law provides such a right. Actually, this is one of the options when a male or female pensioner cannot show official earnings in full before retirement.

Either spouse has the full right to a tax deduction. Family relationships must be officially recorded. The applicants have marriage certificates and maintain common affairs and a common household.

This gives the right to receive benefits from the state, since, in fact, such discounts are provided not to a specific citizen, but in his person - to the family of a pensioner.

Tax deduction for military pensioners

In fact, it is not provided to this category of citizens. A tax refund when purchasing an apartment is possible only when the personal funds of a military person or a person equivalent to a military personnel were invested in the purchase of housing.

In this case, the deduction for the apartment is the same 13% of the contract price, but in this case the amount of costs is determined based on the citizen’s personal investment. That is, if the apartment cost 1 million rubles, and 300 thousand of them were paid by the applicant, then it is from this amount that he has the right to count on compensation. As in other cases, a declaration is submitted, a package of documents confirming ownership is drawn up, which must specifically indicate the share of investment of personal funds, as well as obtaining the right of personal ownership of housing.

These payments, if verified by the tax service, are paid from the next year after filing the application.

Application deadlines

Citizens have the right to apply for a tax deduction after acquiring ownership of real estate within the next year or later. However, receiving it for the periods following it for non-working pensioners who do not have income is not relevant. The legislator provided for this and granted this category of citizens the right to receive money not only for the year in which the property was acquired, but also for the 3 previous periods.

In practice, this means that if, for example, property was purchased in 2020, then the citizen receives a deduction both for this year and for 2020, 2020, 2020. However, it should be borne in mind that the later the pensioner applied for the deduction, the shorter the period he can receive it. That is, if he files a declaration in 2020, then no money will be paid to him for 2020.

Social tax deductions for pensioners who continue to work

Social tax deduction is guaranteed for working pensioners on a general basis, as for any other working citizen of the country. This means that the maximum amount of tax social deduction is limited to a limit of 50,000 rubles, and in total no more than 120,000 rubles.

Social tax deductions are due for the following types of payment:

- for own education and education of children under 24 years of age;

- under a non-state pension insurance agreement in the amount of the insurance amounts paid;

- in the amount of additional insurance premiums for the funded part;

- in the amount of contributions under a voluntary life insurance contract when concluding a contract for at least 5 years;

- for the services of medical organizations (including for medicines purchased at one’s own expense)

Important! If the treatment is expensive and is included in the legislative register, then reimbursement of expenses occurs in full without taking into account the established limits.

Tax deduction for treatment and sanatorium rehabilitation is the most popular type. Conditions that must be met:

- the payment was made with the pensioner’s own funds;

- the medical organization has a license to operate and pays taxes;

- medicines are included in the official register;

- all expenses spent can be documented;

- the type of medical service is included in the register.

Another type of popular deduction is the tuition deduction.

Conditions for receiving this type of deduction:

- the organization must have a license to conduct educational activities;

- there is an agreement for the provision of paid services;

- Tuition costs can be verified.

Among the types of training are:

- tuition at a university on a paid basis;

- obtaining a license at a driving school;

- training at paid trainings and seminars;

- studying of foreign language.

Important! The deduction can be issued not only for your own education, but also for parents and children.

Can they refuse payment?

In some cases, tax authorities may refuse to pay a tax deduction.

Among them it should be noted:

- lack of grounds for providing benefits;

- factual errors when filling out the declaration;

- existing debts to the Federal Tax Service;

- expiration of the deadline for providing a deduction.

Reference! The refusal of the tax authorities to pay can be appealed in court.

In accordance with the law, a number of citizens, if there are grounds for this, are provided with benefits for paying fiscal fees in the form of a tax deduction. At the same time, even non-working pensioners who in fact do not have any taxable income have the right to receive it. This is possible due to the mechanism of transferring tax deductions, when they are returned the funds paid for the 3 years preceding the year of acquisition of real estate.

Transferring deductions for a pensioner to previous years

The right to a property deduction occurs after obtaining ownership of housing. For the DDU, this is the moment of transfer of the apartment under the Transfer and Acceptance Certificate, and for the purchase and sale agreement, this is the moment of state registration of ownership.

After the entry into force of Federal Law No. 330-FZ of November 21, 2011, Part 2 of Art. 220 of the Tax Code of the Russian Federation, and from January 1, 2012, benefits were introduced for pensioners . Yes, there must still be ownership of housing, but now pensioners can receive a property deduction for the previous three years , regardless of when exactly ownership was obtained. This means that the pensioner’s deduction will include the years when he was still working.

We read paragraph 10 of Art. 220 Tax Code of the Russian Federation:

“For taxpayers receiving pensions in accordance with the legislation of the Russian Federation, property tax deductions provided for in subparagraphs 3 and 4 of paragraph 1 of this article may be transferred to previous tax periods, but not more than three, immediately preceding the tax period in which the carried forward balance was formed property tax deductions."

Thus, a pensioner can receive a deduction for four years, counting the year in which the non-carryover balance arose.